Pre-Seed Investing & Risk

At our annual LP meeting this past fall, we gave a short talk on how we think about pre-seed investing & risk, and why we think there’s a particularly interesting risk:reward at this stage.

We’re sharing this broadly with the community in order to spark a larger discussion. Slides are here.

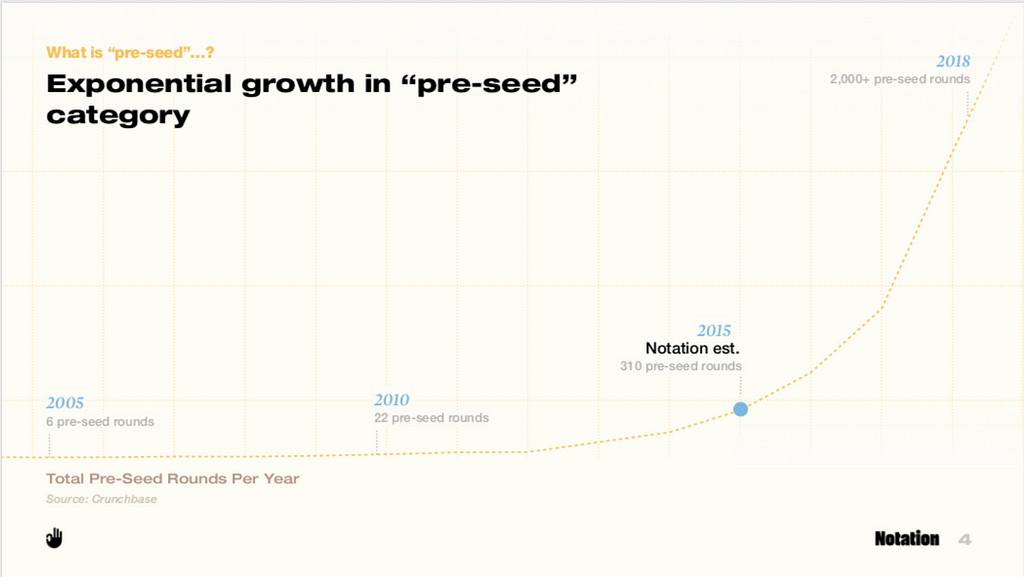

Over the course of the past five years, “pre-seed” rounds have gone from a nebulous sounding name into a full-blown category. When Notation was formed in early 2015, there were many questions about pre-seed — namely, whether or not ‘pre-seed’ rounds were here to stay, and confusion around what exactly the terminology meant. Fast forward to today, and we’re seeing more than 2,000 pre-seed rounds being funded each year, and more and more funds dedicated purely to this stage.

One simple explanation for the rise of ‘pre-seed’ rounds is just that round sizes have shifted, and that pre-seed is simply the new seed round. There’s some truth to this, but we think it’s more than that. Aside from defining pre-seed as a round size, we think about pre-seed as a type of risk, and a way of working with founders, specifically on go-to-market.

We also believe that for those firms and investors with the right skillset, it’s a type of risk that’s well justified, given where valuations are at pre-seed compared to other stages like seed and Series A, which are often exponentially higher. At Notation, we work with technical founding teams in the trenches on day 0:00. At day zero, the degree of risk sits at a startup’s highest point, whereas valuation is (presumably) at its lowest. With each stage of funding, that risk curve starts to trend downward, whereas the valuation curve trends upwards.

So if the valuation curve is something determined by the market, the question then becomes: what does each investor believe the risk curve looks like?

Here’s what we think:

If you examine the chart above, you’ll notice a couple of important details about how we think about the risk curve. First, we don’t think that it’s linear; second, we don’t think that a startup is meaningfully de-risked until Series A or even Series B or later. And so what this means to us is that for each individual startup, we should maximize the amount of risk we take, and thus invest the bulk of our capital at the pre-seed stage — which is what we do.

That said, not all early-stage company risk is created equal: there are risks we’re happy to take (and even maximize), and then there are certain risks we avoid at all costs. For example, we embrace early-stage go-to-market risk and product risk and even some technical risk, but we don’t take team risk, and we don’t love funding idea discovery. We also believe that there are ways we can actively participate in the de-risking process: at a portfolio level, through smart portfolio construction and a disciplined approach to valuation and ownership; and then also at the individual company level, by actually helping out and bringing value-add advisory services to the founders we partner with.

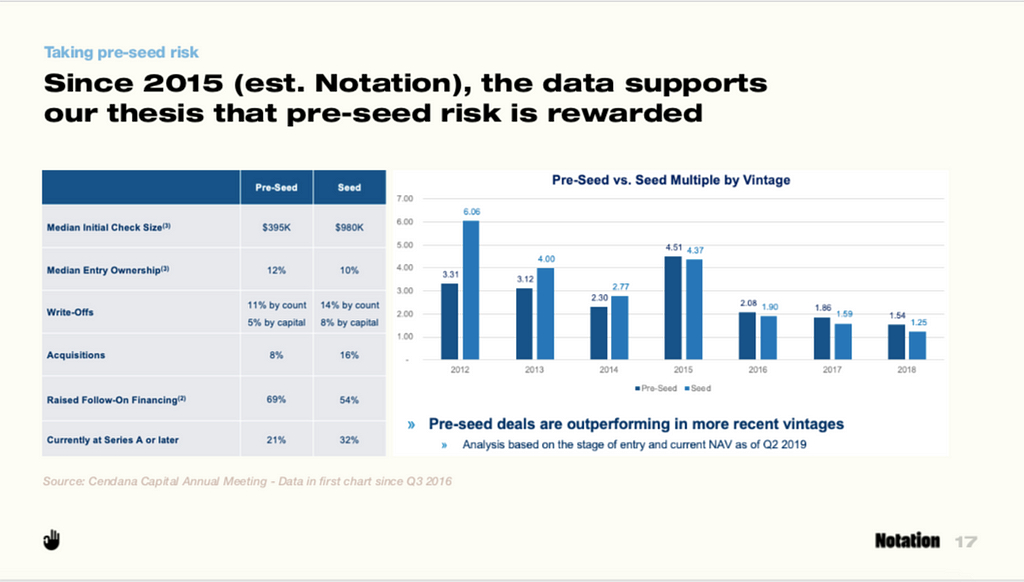

As dedicated pre-seed investors, we know that the failure rate for super early-stage startups will be higher than many of our peers that invest at later stages — and of course no one feels this more acutely than the founders we work with. This can feel like a daunting task, and at times really messy. But we love the actual work, rolling up our sleeves and being in the trenches with founders to solve these early, but impactful challenges. Ultimately, we believe that the reward greatly outweighs the risk compared to other stages across the venture stack. The early data is beginning to support our thesis too, as one can see from the chart below, kindly provided by our partners at Cendana Capital.

So this is how we think about pre-seed: not as a specific investment size or even a new category, but a pursuit of calculated (and justified) risks. We’d love to hear how others think about it too 🙂

We’re always available at hello@notation.vc and you can follow us on twitter or get updates here.

Alex, Nick, Katherine and Thomas

Pre-Seed Investing & Risk was originally published in Notation on Medium, where people are continuing the conversation by highlighting and responding to this story.